We explore UCT case highlights and practical takeaways from 2025.

Unfair contract terms remain a key regulatory enforcement priority

Unfair contract terms (UCT) remained in the regulatory spotlight in 2025. Following the introduction of significant penalties for UCT in November 2023,[1] there has been heightened UCT enforcement by both ASIC and the ACCC. In May 2025, the Court imposed a fine of $750,000 on HCF Life for using a misleading term (under appeal in relation to findings of UCT with a court hearing listed for 11 March 2026) and in June 2025, the Full Court delivered the appeal judgment in ASIC v Auto & General Insurance. Meanwhile, the ACCC accepted a number of notable court enforceable undertakings related to UCT including from Mable Technologies Pty Ltd.

Key takeaways for businesses

Courts and tribunals are shedding light on when terms in standard form contracts will be ‘unfair contract terms’. This involves considering the boundaries of what is ‘reasonably necessary’ to protect legitimate interests and what crosses the line into creating significant imbalance, consumer detriment and opacity.

Some key takeaways from recent decisions relate to the following types of clauses:

- Dispute resolution clauses:

- Clauses that provide for commercial arbitration and restrict the resolution of disputes through courts or class actions may be unfair and void under the UCT regime. This is the case even if the same dispute resolution process applies to both parties. Arbitration clauses are particularly likely to be unfair if:

- arbitration is impractical due to cost (e.g. because the cost of arbitration is disproportionate to the potential value of a claim); and/or

- the clause is not sufficiently transparent to consumers (e.g. if it is buried in a long document).

- Fee/price escalation clauses:

- Use proportionate, evidence-based formulas, avoid ‘double counting and be ready to substantiate each component with financials.

- To justify that price escalation rights are reasonably necessary, be prepared to produce detailed financials (e.g. revenues, cost structures, margins, capital plans, funding capacity) and reasoned analysis linking each element of the formula to a legitimate need.

- Discretion afforded unilaterally to one party is relevant to the assessment of unfairness.

- Transparency helps but cannot cure substantive unfairness. Even if a formula is clearly drafted and pre-disclosed, transparency alone will not save a term that is unfair.

- Insurance notification clauses:

- Terms requiring insureds to notify material changes to the risk insured are less likely to be considered unfair. Including specific examples of the types of things that should be notified is also helpful.

- Always consider the ‘reasonable consumer’ in standard consumer contracts and how they would interpret the provision based on ordinary language in the context of the contractual documentation as a whole – including that the consumer may not be aware of the various implied duties and other restrictions on insurers under the Insurance Contracts Act 1984 (Cth). – Because of the reliance on this Act, the findings in this case may be limited to insurance contracts.

- Clauses that provide for commercial arbitration and restrict the resolution of disputes through courts or class actions may be unfair and void under the UCT regime. This is the case even if the same dispute resolution process applies to both parties. Arbitration clauses are particularly likely to be unfair if:

Below, we summarise these cases and the key implications for businesses.

AghaeiRad v Plus500AU (December 2025)

Court: Federal Court of Australia

Background

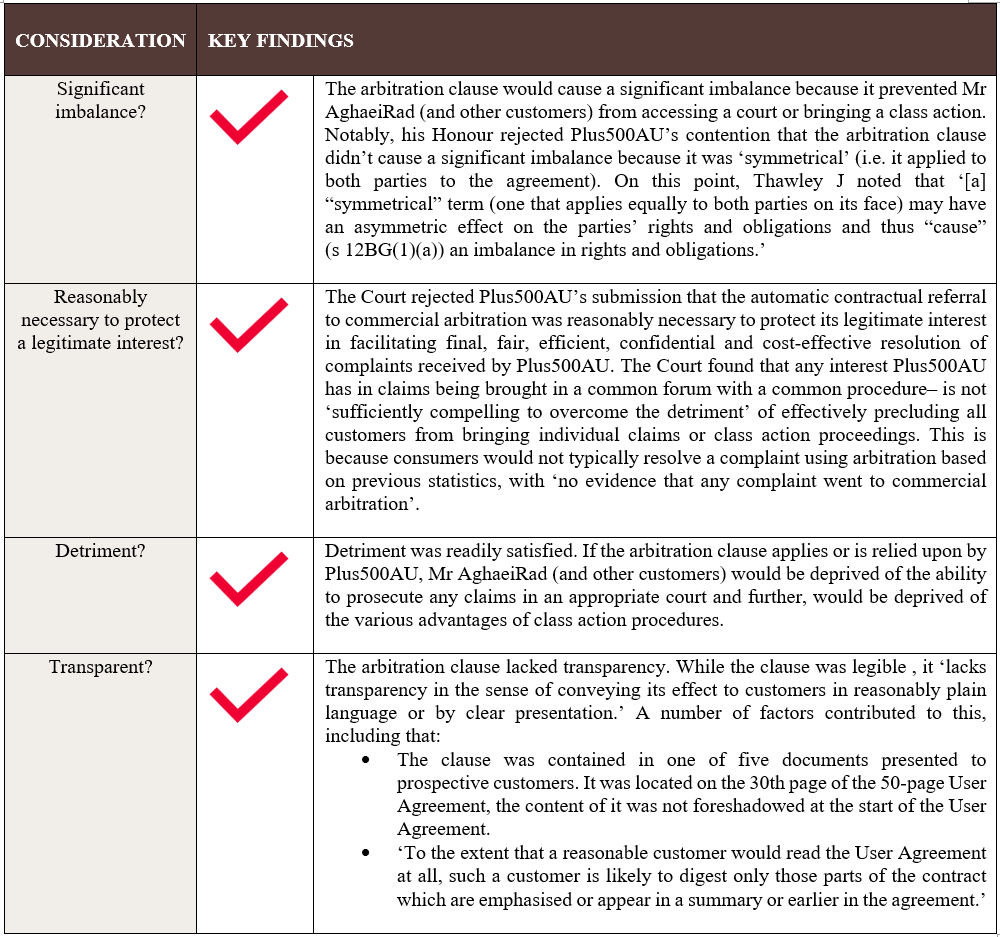

Mr Ali AghaeiRad traded on Plus500AU’s online trading platform for over-the-counter ‘Contracts for Difference’. After almost a year of trading, Mr AghaeiRad lost all the money he had deposited into his trading account – $111,948. Mr AghaeiRad brought proceedings against Plus500AU, contending – among other things – that the clause was void as an unfair contract term under section 12BF of the ASIC Act.

Impugned term (‘Dispute Resolution’ clause)

The impugned arbitration clause outlined a tiered dispute process with defined timelines: all reasonable endeavours to resolve, then escalation to Senior Officers after 5 business days for a further 10 days of good faith negotiations. If unresolved, either party may require mediation (costs shared), and if not settled within 30 days (unless extended) the dispute proceeds automatically to arbitration under the Resolution Institute Arbitration Rules.

Court findings

For a more detailed summary of AghaeiRad, see ‘Symmetry vs. Substance: Unfairness in Arbitration Clauses after AghaeiRad v Plus500AU’.

Anderson v Kincumber Nautical Village Pty Ltd (September 2025)

Tribunal: NSW Civil and Administrative Tribunal (D Robertson, Principal Member).

Background

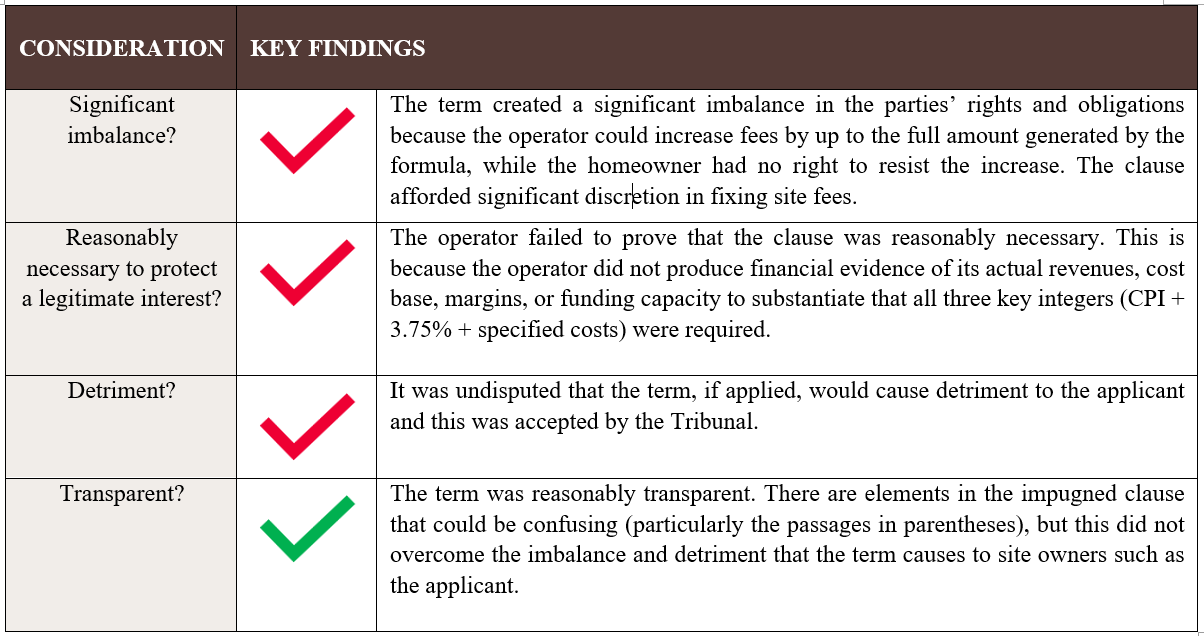

Mr Anderson was a resident of the Kincumber Nautical Village (a residential land lease community). In November 2023, the operator of the land lease community notified an increase to Mr Anderson’s weekly site fees from $229 per week to $268 per week, based on a ‘fixed method’ fee escalation clause in the site agreement. Mr Anderson challenged this fee increase, alleging that the clause governing fee increases was an unfair term under the ACL and therefore void, and sought refunds of overpaid site fees.

Impugned term (‘Fee Escalation’ clause)

The impugned term contained a fee escalation formula whereby site fees would rise every November regardless of start date, with any missed increase ‘caught up’ at the next review. The uplift fee would be the sum of any positive change in the CPI, plus 3.75%, plus a proportional share of specified operator cost increases and any GST change, rounded up to the nearest dollar.

Tribunal findings

The Tribunal held that the ‘Fee Escalation’ clause was unfair and void.

ASIC v Auto & General Insurance (June 2025)

Court: Full Federal Court (Derrington, O’Bryan And Cheeseman JJ).

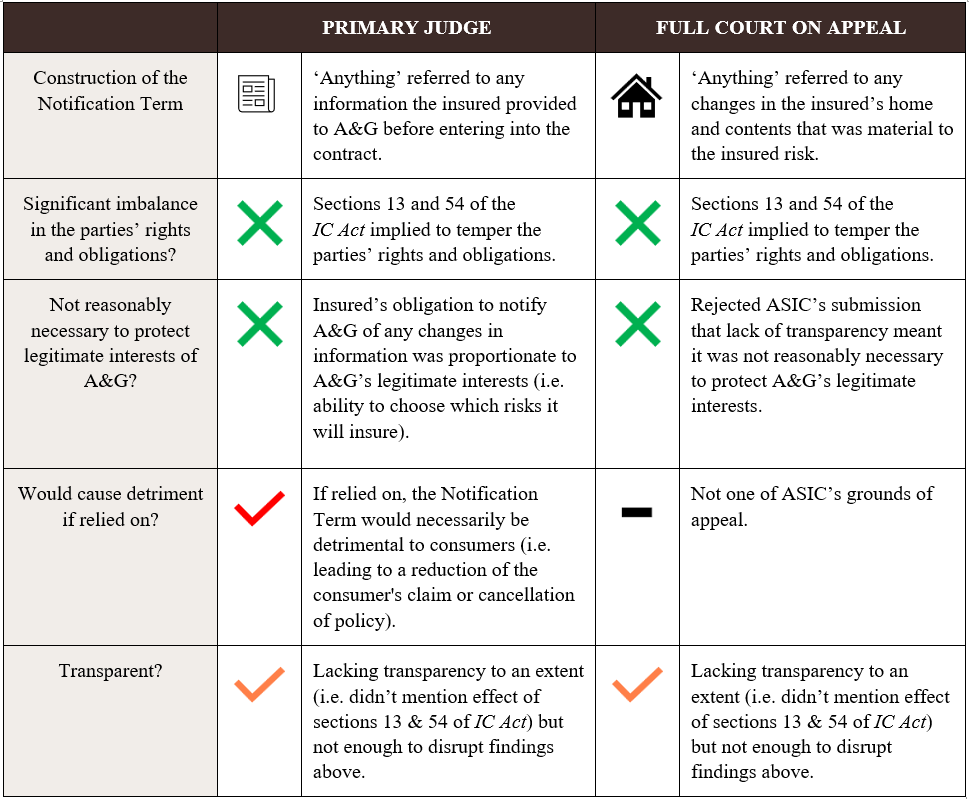

Impugned term (Notification Term)

The impugned ‘Notification Term’ contained in a standard consumer home and contents insurance PDS (forming part of an insurance contract) mandated that customers ‘tell us if anything changes while you’re insured with us’ regarding their home or contents, and included specified examples of the types of things that should be notified.

Court findings

As we explored in a previous blog post, the Court found that the ‘Notification Term’ was not unfair under s 12BF of the ASIC Act. Below is a summary of key findings of both the primary judge and the Full Court of the Federal Court on appeal.

[1] As of November 2023, the maximum penalty for corporations is the greater of $50 million, three times the benefit obtained, or 30% of adjusted turnover.